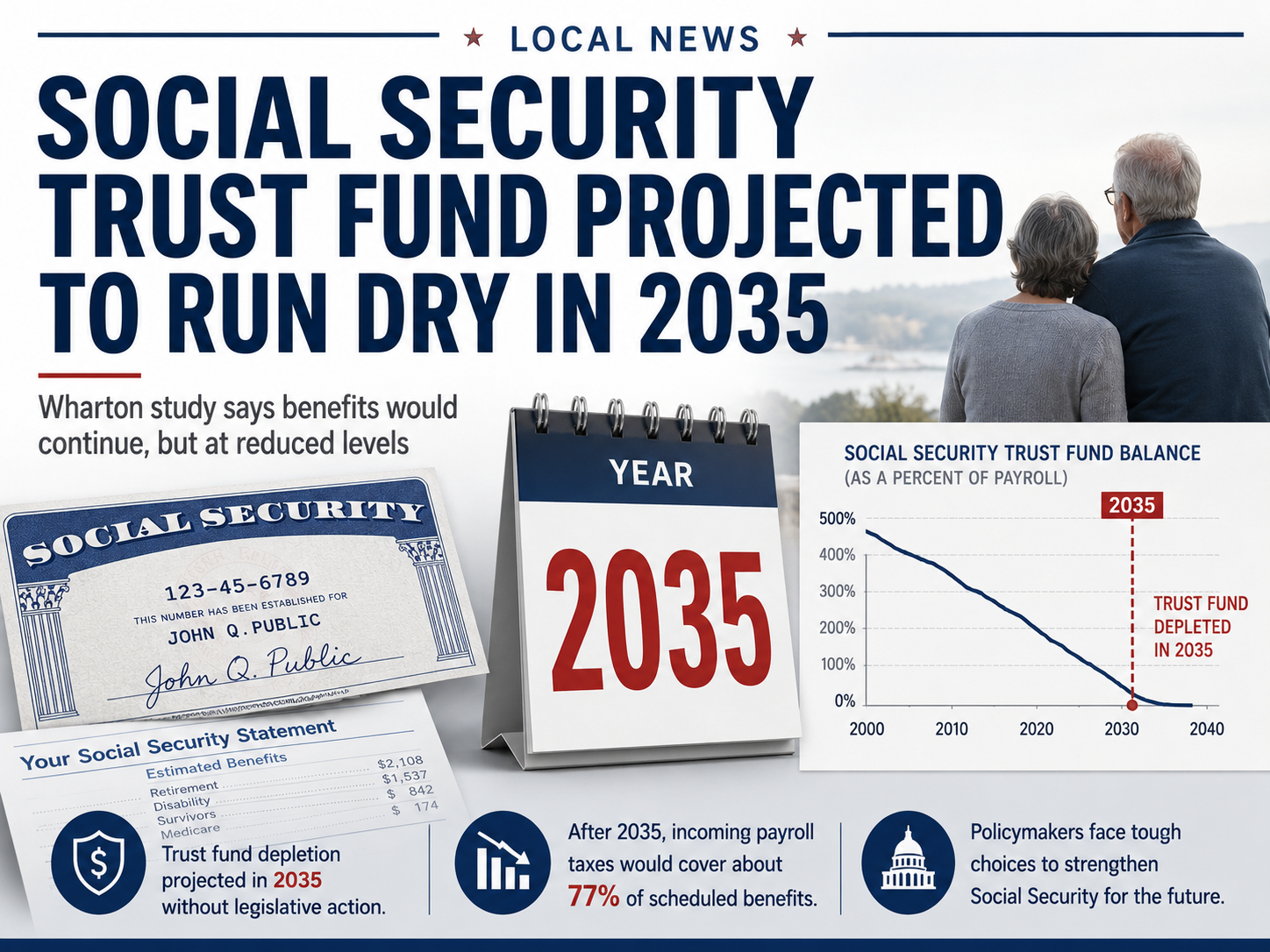

A new independent analysis from the University of Pennsylvania’s Penn Wharton Budget Model projects that Social Security’s combined trust fund will be depleted by February 2035, a finding that carries direct implications for millions of Americans who depend on the program, including retirees and working families in York and Lancaster counties.

The projection, published June 11 by researcher Seul Ki (Sophie) Shin under the direction of faculty director Kent Smetters, arrives at a conclusion close to the Social Security Administration’s own 2026 Trustees Report, which projects depletion in the third quarter of 2034.

What Depletion Would Mean for Beneficiaries

Depletion does not mean Social Security would disappear. Under current law, benefits would be reduced to the level that can be paid from ongoing payroll tax revenue collected in that same year. The Penn Wharton Budget Model projects that 86 percent of scheduled benefits would be payable at the time of combined fund depletion, falling to 60 percent by 2100. The Social Security Administration’s Office of the Chief Actuary projects a slightly lower 83 percent payable at depletion, with 65 percent payable by 2100.

For a York County retiree currently receiving $2,000 a month from Social Security, a 14 percent automatic reduction at depletion would translate to roughly $280 less per month, with deeper cuts projected in later decades.

Closing the projected shortfall would require raising the combined employer and employee payroll tax rate from 12.4 percent to 17.1 percent, an equivalent reduction in benefits, or some combination of both.

The 75-Year Picture

Penn Wharton projects a 75-year actuarial deficit of 4.65 percent of taxable payroll, compared with 4.42 percent in the 2026 Trustees Report. The difference of 0.23 percentage points is modest, and researchers say the close alignment between an independent bottom-up model and the government’s top-down estimate strengthens confidence that Social Security’s financial problems are real and not the result of overly pessimistic official assumptions.

Penn Wharton is the only non-governmental group that produces independent long-range projections of Social Security’s finances. Unlike the government’s approach, which begins with assumptions about aggregate trends, Penn Wharton’s microsimulation model builds its forecast from individual-level data on earnings histories and family structures.

Fertility and Longevity Drive Key Differences

The similar overall bottom lines between the two projections mask significant differences in the underlying assumptions about population trends.

Penn Wharton projects lower long-run fertility at approximately 1.6 births per woman, while the Trustees assume fertility recovers to an ultimate rate of 1.75 by mid-century. Fewer children born today means a smaller taxpaying workforce in the 2040s and beyond, which would accelerate Social Security’s financial strain in the second half of the century.

On the other side of the equation, Penn Wharton is more conservative than the government about how much longer Americans will live. By 2100, the Trustees project life expectancy at age 65 of 22.6 years for men, a gain of 4.4 years. Penn Wharton projects much smaller gains of 1.6 years for men, reaching 20.0 years. Shorter average benefit collection periods reduce projected program costs, particularly through the middle decades of the century, before lower fertility pushes costs higher.

The researchers note that broader adoption of GLP-1 drugs, particularly among lower and median-income households, could lead Penn Wharton to revise its longevity projections upward in future analyses.

An External Check on Official Numbers

The Penn Wharton researchers say the agreement between their independent model and the government’s own report carries a specific significance this year. The analysis notes that it provides an external check on whether the economic outlook underlying the official estimates became too optimistic following passage of federal fiscal legislation in July 2025. The researchers concluded that the close alignment between the two projections offered no support for concerns that official figures were overstating Social Security’s financial health.

Congress has not acted on any comprehensive reform to address the projected shortfall. Proposed fixes have ranged from raising the retirement age and adjusting the benefit formula to lifting the cap on wages subject to payroll taxes.

The Penn Wharton Budget Model full analysis, including downloadable data tables, is available at budgetmodel.wharton.upenn.edu.

Sign up for our Sunday Spectator. Delivered to your inbox every Sunday, with all the news from the week.

Thomas Hyslip lives in Tega Cay with his wife and daughter. After 27 years in the U.S. Army and Federal Law Enforcement, he retired to pursue his passion for teaching. Tom is now an Assistant Professor of Instruction at the University of South Florida. In 2 short years he has won 10 awards from the South Carolina Press Association, including first place in column writing, education beat reporting and best podcast.